Becoming a homeowner isn’t as difficult as it once was. Today, there are programs that assist with down payments for homes and the Federal Housing Administration (FHA) offers mortgage financing with just 3.5% of a home selling price as a down payment, a much lower threshold than the 20% down required in many traditional home loan arrangements. But getting approved for a mortgage requires two very important criteria to be met: Financial qualifications, in other words, how much you earn; and credit requirements. In other words, how reliably you pay your bills.

The first step is often outside of our control: Money. We are paid what we earn. Sometimes however a second job or freelance gig may be necessary for us to be able to afford a new home purchase but keep in mind that if you pursue a secondary gig in order to boost your income and to potentially qualify for a mortgage, you will have to be able to prove that income so keep your financial records in a safe, easily accessible place because it will be needed once you apply for a loan.

Making sure you are able to afford a home has to be the first step prior to applying for a mortgage loan since it makes no sense to try to buy something you don’t presently have the ability to pay for. All bank lenders will require proof that you can make your mortgage payments on time and in order to do that, they will require paycheck stubs and tax documents and also even bank statements as proof of your income and also to determine whether you are within a prospective lender’s debt-to-income ratio requirements (DTI).

Your DTI is the amount of income you have compared to the bills you have to pay. The lower your debt to income ratio is, the higher your chance of getting approved for a mortgage.

Most lenders look for 36% or less, though up to 43%–50% is acceptable for some conventional or FHA loans. A lower DTI indicates to lenders a stronger ability to manage payments, with 43% being a common maximum for conventional loans.

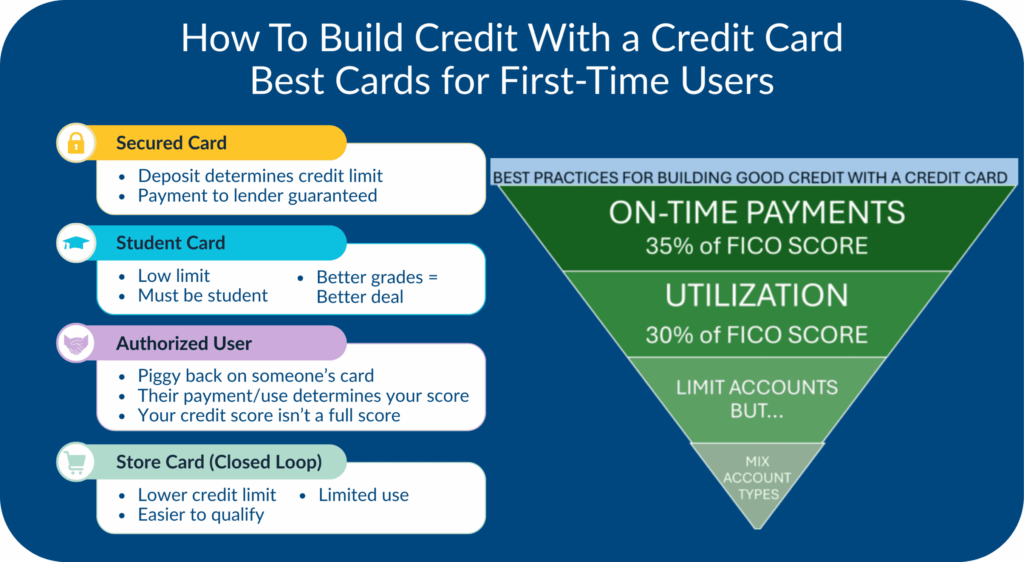

If you have bad or even no credit, a good place to start on the pathway to improving your credit standing is a credit card. If you can’t get approved for a standard credit card, then a secured card is the next best and most effective option. A secured card will require you to put up a usually refundable security deposit ranging from $100-$500 but the card issuer will report your payments on the card to any or all of the major credit bureaus, thereby helping you establish a credit history. Credit is the major obstacle outside of funding to secure a home loan. Use credit wisely.

Officially, the FHA requires a minimum credit score of 580 to be approved for one of its loan programs; in reality however, most lenders want to see your credit score at or above 620. In order for you to get there, its essential you start not only working on building or rebuilding your credit, but monitoring your score closely as well. Credit Karma, Credit Sesame, and WalletHub are reliable credit monitoring and improvement resources and they are free to use.

Acquring a good credit score means paying your bills on time and avoiding taking on credit you don’t need. In evaluating your credit for a mortgage loan, lenders will want to see that you have not overextended yourself or have significant debt. Keep your balances as low as possible. Pay on time. A rule of thumb is never letting a payment go past 30 days late; that goes on your credit as a missed payment and it can adversely affect your score and your ability be approved for a home loan.

Keep in mind that credit repair companies do not typically do more than what a determined person with bad credit can do and there is a risk that doing business with some credit repair businesses could expose you to fraud, theft, or illegality; some of these “credit fixers” have at times been accused of ripping people off. In any case, building credit can be done safely and legally by applying common sense principles to your bill paying and credit building.

There are a number of resources available to further inform and assist you in your credit building and home purchase journey. Just browse the web and do your research. Good Luck!